See Before you Owe try a collection of mortgage instructions away from an individual Monetary Safety Agency (CFPB). It suggests mortgage hunters this new methods they need to simply take to start and you will handle a home loan account. It offers more information to your interest rates, and demonstrates to you what are similar sales on finance, also.

This is going to make sense. Home hunters should know what they are joining. And who wants gotcha times or abrupt clarifications immediately after it seems (or actually is) too-late in order to straight back aside?

Thus, the mortgage lender lawfully have to supply the borrower a proper set from closure disclosures at least three working days in advance of closing day.

Improved Disclosure Materials: A reaction to the mortgage Drama Fallout.

See Before you could loans with no credit check in Goodwater Are obligated to pay support consumers know both the mortgage processes, as well as their options. The brand new CFPB, a federal company, works to remain lending methods fair to possess regular people. From the agency’s own terminology: We help in keeping banking institutions and other monetary suppliers consumers count on each date operating pretty.

Up until the most recent Understand Before you could Owe package was created, there had been four disclosure variations. They certainly were not very very easy to realize, or to fool around with.

You to changed pursuing the houses drama that unfolded ranging from 2007 and 2010. Actually, the newest federal financial laws itself changed.

This current year, the new Dodd-Frank Wall Roadway Reform and you will Individual Cover Work led lenders so you can make credit conditions stricter, so you can reduce the threats so you’re able to individuals. From the 2015, new CFPB had its first Discover Before you could Owe publications. They simplified the borrowed funds revelation content your lenders needed to render the borrowers.

Financial Disclosures Are simple to Understand, User friendly-And Individualized to own Mortgage Customers.

Today, the newest CFPB website boasts the Home ownership area. Which an element of the web site courses brand new upbeat loan borrower owing to the mortgage-looking to thrill. It has got info, recommendations, and you may notice.

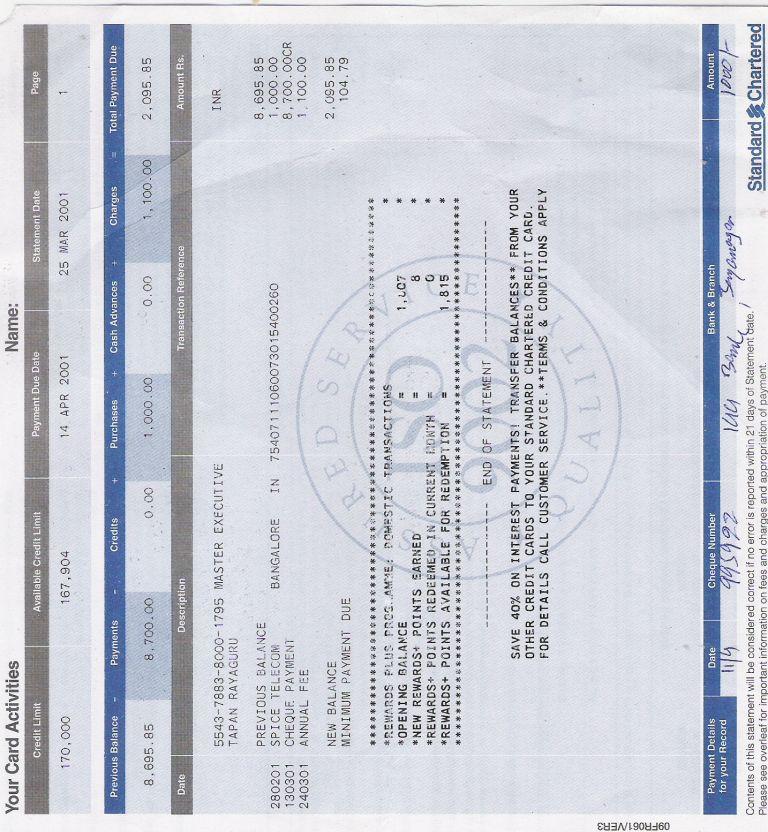

- The borrowed funds Guess. This proves new arrangement the customer try and make – information on the borrowed funds and all of the relevant fees. It states the speed, and you may if that is closed from inside the. In case your terms discipline individuals whom pay their monthly number very early, this document says very. Most of the advised, the borrowed funds Guess may help that loan candidate know exactly what’s available, after that check around and you will contrast readily available mortgages within the last occasions prior to closing day! See what that loan Guess works out.

- The fresh Closure Disclosure. This helps your avoid high priced unexpected situations during the closing desk. Does the borrowed funds Guess satisfy the Closure Disclosure? The toolkit reveals an individual just how to contrast which document – its number and you may loan conditions – into the exact same details where they appear on Mortgage Guess. The new borrower gets about three business days evaluate this type of variations and you can ask questions before-going completed with the latest closure. See what a closing Revelation ends up.

Our home Mortgage Toolkit gets borrowers the mandatory perspective understand these disclosures. And also the mortgage lender gives one for every single borrower. See just what our home Financing Toolkit (PDF) works out.

See Their Rights, and you may Understand the Legislation, new CFPB Claims

Contemplate, all financial borrower is actually entitled to an ending Revelation at least about three business days in advance of this new deed import. This may feel like a pain in the neck for an optimistic consumer went towards the finishing line. However,, too today see, there is certainly a consumer-friendly rationale for the around three-time months. It allows people adjust the heads regarding the closing in the event the something’s significantly less guaranteed. It gives a-flat go out when a house visitors might get clarifications on the process and terminology, describe any queries otherwise distress, and maybe even consult changes to the home loan agreement.

At that time, the agency’s online book can be very of good use, for even an experienced customer. It gives worksheets, finances variations, and even sample role-to try out scripts the buyer can use to prepare for real discussions to your mortgage company.

In addition it tells members what mortgage con are, and why not to get it done. Stating well-known? Yes, but some some one do fudge wide variety, very perhaps they are doing must be told it’ll most likely perhaps not stop really!

Financial People Need Accept Applicants for the an unbiased Ways. Therefore Must The App!

For the , the fresh CFPB issued suggestions in order to loan providers for the playing with formulas, as well as fake cleverness (AI). Cutting-edge technical helps make all sorts of user data available to loan providers. These companies should be capable articulate and this study forms their choices. They can not merely state the fresh new AI did it. So that the suggestions warns lenders to not ever merely mark packages to the models without stating this factors, in for every single case, once they turn people off for mortgage loans. If they never stick to this guidance, he is offending the fresh federal Equivalent Borrowing from the bank Possibility Act. In reality, this new Equivalent Credit Possibility Operate needs lenders so you’re able to establish the precise reasons for having refusing so you’re able to material financing.

What makes that it? Because when our lenders inform us straight-right up as to the reasons we are deemed ineligible, upcoming we could can proceed down the road, and you will increase all of our borrowing reputation properly. And, they reassures you you to definitely unlawful bias is not inside play. Its hence your CFPB states the lending company need condition brand new in depth findings you to went to your assertion. Put another way: The items did the latest candidate perform or perhaps not perform?

Including, the newest CFPB says within the release titled CFPB Circumstances Ideas on Credit Denials because of the Loan providers Playing with Artificial Cleverness, a loan provider have to straightforwardly display how come, it does not matter the applicant might be surprised, disturb, otherwise angered to determine they have been are graded to your data that can not naturally interact with their money.